A simple way to protect employees from extreme rainfall

When a qualifying event occurs, eligible enrolled employees may receive a payout directly, typically within about a week after the trigger is confirmed and payout details are received.*

See how it works

An easy, predictable process

Ric is designed so employers, brokers, and employees can understand how it works in minutes.

Step 1:

Employer offers Ric

Employers add Ric as a benefit and choose how it’s funded: employee-paid, employer-paid, or shared.

Step 2:

Employees choose a tier

During enrollment, employees select their payout level. Ric uses a clear two-tier structure, so employees always know what they pay — and exactly what they’ll receive if a qualifying rainfall event occurs. Pricing reflects expected event frequency in a given area and the payout amount selected. No hidden fees. No surprise adjustments.

Step 3:

Ric monitors rainfall

Ric tracks extreme rainfall at covered locations using trusted third-party data against a trigger set in advance. No claims. No photos. No proving damage.

Step 4:

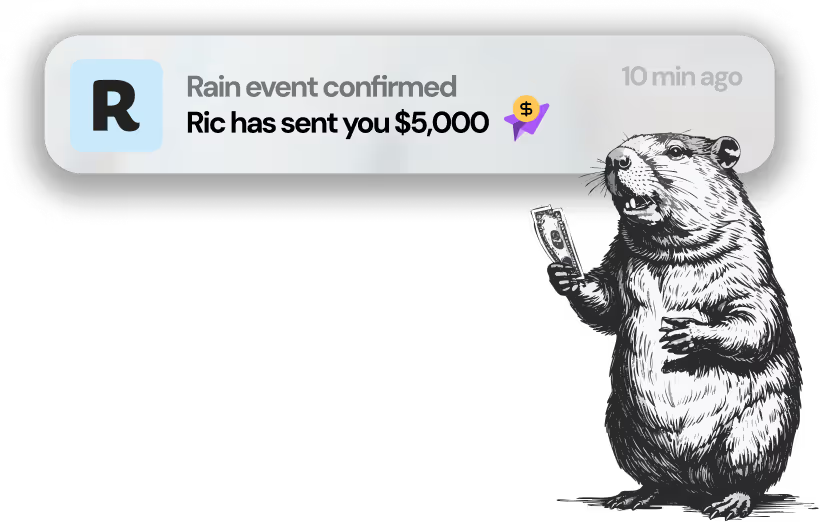

Trigger met → payouts go out

When rainfall reaches or exceeds the trigger, Ric confirms the event and sends payments automatically based on each employee’s tier. Funds typically arrive within about a week, and employees can use the money however they need.*

Why this matters

Extreme rainfall disrupts work and home life nationwide, and many employees don’t have reliable coverage for the costs that follow. Ric fills that gap with a pre-agreed trigger and a fixed cash payout — delivered quickly — so employers can support faster recovery and workforce stability.

Protection for renters and homeowners alike

Ric follows people, not property. Coverage doesn’t depend on owning a home, having a mortgage, or carrying traditional property insurance.

If an enrolled employee is in a covered location and the trigger is met, they receive the payout based on their selected tier — making Ric especially valuable for renters and working families often left out of other protection.

Protection for renters and homeowners alike

Ric follows people, not property. Coverage doesn’t depend on owning a home, having a mortgage, or carrying traditional property insurance.

If an enrolled employee is in a covered location and the trigger is met, they receive the payout based on their selected tier — making Ric especially valuable for renters and working families often left out of other protection.

Available in all 50 states

One benefit strategy for your full U.S. workforce — wherever employees live and work.

FAQ about how Ric works

Is Ric the same as homeowners or flood insurance?

No. Ric does not replace homeowners, renters, or flood insurance. It is an extra layer of financial protection that pays employees when extreme rainfall at covered locations reaches an agreed trigger, no matter what policies they have.

Is this only for people who live near the coast?

No. Ric is designed for communities across the country. Extreme rainfall events have affected inland cities, suburbs, and small towns, and employees in those places often face the same financial stress as coastal residents.

Do employees need to own a home to be covered?

No. Employees do not need to own a home. Renters and homeowners are treated the same. If they are enrolled, located in a covered area, and the trigger is met, they are eligible for a payout based on their tier.

How do employees get paid after a qualifying rainfall event?

Ric verifies the rainfall event using trusted weather data, then sends payments directly to enrolled employees. They affirm with an affidavit that they’ve had a physical or financial loss. Funds usually arrive within a week of the event.

What can employees use the money for?

They can use it for whatever matters most at the time. Common examples include rent or mortgage payments, temporary housing, transportation, childcare, replacing essentials, or covering lost income.

Does Ric coverage move with employees if they change addresses or jobs?

If an employee changes jobs, they can enroll again if their new employer offers Ric. If they move, the policy is updated or reissued so their rainfall threshold reflects their new location.

What happens if there is heavy rain but no official damage to the property?

Ric does not require proof of damage at a specific home, losses can be financial in nature. If the measured rainfall at a covered location reaches or exceeds the agreed trigger, enrolled employees receive their payout.

How is this different from government disaster aid?

Government aid can be limited and often takes weeks or longer to arrive. Ric is a private benefit offered through employers that pays a fixed amount quickly after a qualifying rainfall event, so employees have money on hand while they wait on other sources of help.